📐 "First 50 Enterprise Queries Get Custom 3D Warehouse Design" Plan

Unlock Growth: Zero-Capex Industrial Racking to Boost Storage Now & Pay Over Time

For businesses across the globe, from the bustling manufacturing hubs of Southeast Asia to the rapidly expanding logistics corridors of the Middle East and Latin America, a single, persistent challenge stifles growth: the prohibitive upfront cost of modernizing warehouse infrastructure. The traditional path to upgrading storage systems—a significant capital expenditure (CAPEX)—has long been a major roadblock. Companies find themselves trapped, knowing their inefficient storage is costing them money daily in lost labor, wasted space, and missed opportunities, yet unable to justify the large initial investment. This era of compromise is over.

The landscape of warehouse optimization has been fundamentally reshaped by strategic industrial racking financing options. These are not mere loans; they are comprehensive financial engines designed for agility and growth. The concept of Zero-Capex Industrial Racking allows businesses to deploy state-of-the-art storage solutions—from high-density pallet racking and sophisticated mezzanine floors to fully integrated Automated Storage and Retrieval Systems (ASRS) and AGV (Automated Guided Vehicle) fleets—with minimal initial investment.

Companies can now boost their storage capacity and operational efficiency immediately, transforming a crippling capital outlay into a manageable, predictable operational expense (OPEX). This strategic approach to industrial racking financing options is no longer a luxury; it is a critical tool for achieving a competitive advantage, preserving capital, and future-proofing operations.

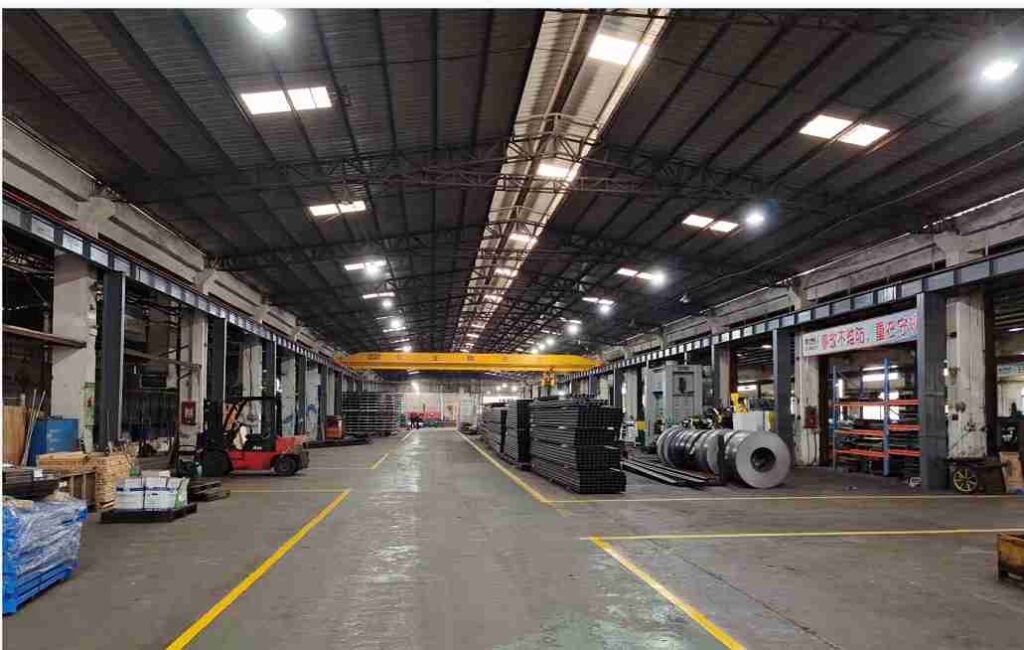

The True Cost of Inefficiency: Why Your Current Storage System is a Liability

Many warehouse operators view their storage systems as a static, depreciating asset. In reality, an outdated or inefficient setup is an active, ongoing liability that silently erodes profitability. The visible cost of new racking often pales in comparison to the hidden expenses of “making do.”

Quantifying the Hidden Drain on Profitability

Labor Inefficiency: In a disorganized warehouse with poor layout, forklift operators and order pickers spend an inordinate amount of time traveling and searching for items. This direct labor waste is one of the largest hidden costs. Implementing a strategically designed system financed through flexible industrial racking financing options can slash travel time, directly boosting productivity and reducing labor costs per order.

Wasted Cubic Air Space: Warehouses pay for volume, not just floor area. Inefficient use of vertical space is like paying for a three-story building but only using the ground floor. Solutions like vertical lift modules (VLMs) or high-rise selective pallet racking, made accessible through tailored industrial racking financing options, allow businesses to fully utilize their building’s cubic volume, effectively increasing capacity without expanding their footprint.

Inventory Shrinkage and Errors: Poor organization leads to misplaced stock, inaccurate counts, and picking errors. These mistakes result in delayed shipments, incorrect orders, customer dissatisfaction, and costly reverse logistics. A modern, systematic storage solution improves inventory accuracy to near 100%.

Safety and Compliance Risks: Overloaded, damaged, or incorrectly installed racking poses a severe safety hazard. The cost of a racking collapse—inventory loss, operational downtime, potential injury, and regulatory fines—can be catastrophic. Professional industrial racking financing options often include expert installation and compliance certification, mitigating this critical risk.

The CAPEX Paralysis: A Common Business Dilemma

The finance department’s mandate to control costs often directly conflicts with the operations team’s need for modern equipment. When a six-figure quote for a new automated conveyor and sortation system lands on the CFO’s desk, it’s often deferred, despite a clear ROI. This “CAPEX paralysis” keeps companies stuck in inefficient cycles. This is the precise problem that modern industrial racking financing options are designed to solve, breaking down the financial barrier and aligning operational needs with fiscal responsibility.

Deconstructing Zero-Capex: A Strategic Financial Model for Modern Warehousing

“Zero-Capex” is a strategic term for a shift in financial modeling. It moves essential storage infrastructure from the capital expenditure (CAPEX) column to the operational expense (OPEX) column, fundamentally changing how businesses budget for and benefit from these assets.

The Operational Lease: Core of Flexible Industrial Racking Financing Options

The most common structure for these solutions is an operating lease. Under this model:

A financial partner purchases the storage system on behalf of the client.

The client uses the system and makes regular, pre-agreed payments.

These payments are treated as an operating expense, fully deductible in the accounting period they are incurred.

At the end of the term, the client typically has options to renew, upgrade, or purchase the system at fair market value.

This structure provides unparalleled flexibility. Exploring industrial racking financing options like this allows a company to preserve its bank lines of credit for other strategic initiatives like market expansion or R&D.

OPEX vs. CAPEX: The Strategic Advantage

Understanding the fundamental difference between these two types of expenditure is crucial for any business leader considering industrial racking financing options.

CAPEX (Capital Expenditure): Involves a large, upfront payment for a long-term asset. It requires significant capital reserves or a loan, depletes working capital, and the asset is depreciated over its useful life on the balance sheet.

OPEX (Operational Expenditure): Involves regular, recurring payments for services or assets used in day-to-day operations. It is 100% tax-deductible in the year it’s spent, is easier to budget for, and preserves cash flow.

By leveraging the right industrial racking financing options, a company can transform a CAPEX-heavy project into a predictable OPEX, freeing up vital capital. This makes advanced technology accessible to a wider range of businesses, not just large corporations.

Beyond Finance: The Multifaceted Benefits of Strategic Industrial Racking Financing Options

The financial flexibility is the headline, but the benefits of this approach create a powerful ripple effect across the entire organization, delivering value far beyond the balance sheet.

Immediate Operational Transformation

The moment a new, optimized system goes live, efficiency soars. For example, implementing a carton flow picking system financed through accessible industrial racking financing options can increase order picking rates by over 60%. Forklift cycle times improve with optimized aisle widths and logical layout. This isn’t a future promise; it’s an immediate, measurable impact on throughput and cost-per-order.

Unmatched Scalability for Growth

Businesses are dynamic, and their storage systems must be too. Traditional purchases lock a company into a static configuration. One of the most powerful aspects of modern industrial racking financing options is their inherent scalability. As a business grows, it can seamlessly add more push back racking bays, integrate additional AGVs, or expand its ASRS capacity, often under the same flexible financial agreement. This allows infrastructure to evolve in lockstep with business demand.

Democratizing Access to Advanced Automation

The revolution in warehouse automation is no longer exclusive to giants. Sophisticated industrial racking financing options make cutting-edge technology attainable. Small and medium-sized enterprises can now deploy:

Robotic Palletizers for efficient loading and unloading.

Automated Sortation Systems for high-speed e-commerce fulfillment.

Unit-Load ASRS for perfect inventory accuracy and high-density pallet storage.

This levels the competitive playing field, allowing smaller players to achieve the same operational excellence as market leaders.

Proactive Risk Management and Enhanced Safety

A new, professionally engineered and installed system is a cornerstone of warehouse safety. Reputable providers of industrial racking financing options ensure that all designs meet stringent international standards (e.g., FEM, RMI), and installation is performed by certified professionals. This proactive approach mitigates the catastrophic risks associated with racking failure, protecting both personnel and inventory.

Identifying the Ideal Candidate: Is Your Business Ready for Zero-Capex Racking?

While beneficial to most, certain business profiles find these industrial racking financing options to be truly transformative.

High-Growth Companies and Startups: Businesses experiencing rapid expansion can scale their physical infrastructure in tandem with revenue, avoiding the cash flow strain of large upfront purchases.

Firms with Seasonal Fluctuations: Companies can design their storage capacity for peak seasons without the financial burden of maintaining underutilized assets during off-peak periods.

Organizations Navigating Economic Uncertainty: In times of market volatility, preserving capital is paramount. These industrial racking financing options allow for essential modernization and efficiency gains without compromising financial stability.

Any Business with an Outdated Warehouse: If the hidden costs of inefficiency are recognized, the business is a prime candidate to explore these modern industrial racking financing options.

A Detailed Portfolio: Storage Solutions Accessible Through Industrial Racking Financing Options

The range of equipment and systems available under these flexible plans is extensive, covering every aspect of modern material handling.

High-Density Storage Systems

Drive-In/Drive-Through Racking: Maximizes storage density for high-volume, low-SKU products by utilizing depth and eliminating multiple aisles. Ideal for cold storage or bulk goods.

Mobile Pallet Racking: Entire sections of racking move on electrically powered rails, creating a single “aisle on demand.” This can increase storage capacity by over 80% compared to static systems, a highly efficient use of space enabled by strategic industrial racking financing options.

Cantilever Racking: The optimal solution for long, bulky items like timber, piping, or furniture. Financing this specialized equipment prevents a niche storage need from becoming a capital headache.

Automated Storage and Retrieval Systems (ASRS)

Mini-Load ASRS: Designed for high-speed storage and retrieval of small parts in totes or trays. Essential for e-commerce, spare parts, and pharmaceutical distribution.

Vertical Buffer Modules (VBMs): A modern evolution, providing ultra-high-density storage and sequencing for production lines or order consolidation.

Automated Material Handling and Robotics

AGV/AMR Fleets: From simple tow tractors to sophisticated autonomous mobile robots (AMRs) that navigate dynamically, automating horizontal transport.

Goods-to-Person (G2P) Systems: Technologies like VLMs and horizontal carousels that bring items directly to the operator, eliminating walking and searching and dramatically increasing pick rates.

The Implementation Blueprint: From Concept to Operational Reality

Executing a successful project financed through industrial racking financing options is a meticulous, collaborative process designed to ensure success and minimize disruption.

Comprehensive Needs Analysis: The process begins with a deep dive into the client’s operations, inventory data, growth projections, and specific pain points.

On-Site Technical Audit: Experts conduct a detailed survey of the facility, measuring space, assessing floor conditions, and understanding current workflows.

Customized System Design & Proposal: Using advanced software, a 3D model of the proposed solution is created, complete with performance simulations and a detailed ROI analysis.

Structured Financial Proposal: Multiple industrial racking financing options are presented, with clear terms, payment schedules, and end-of-term conditions tailored to the client’s financial strategy.

Professional Project Management & Installation: Certified installation teams manage the entire process, ensuring timelines are met, safety protocols are followed, and quality standards are upheld.

Systematic Commissioning & Staff Training: The system is thoroughly tested, and warehouse staff are comprehensively trained on its operation and safety features.

Ongoing Support & Partnership: A long-term partnership is established, offering preventative maintenance, technical support, and consultation for future expansions.

Addressing Key Considerations in Industrial Racking Financing Options

Informed decisions are the best decisions. Here are insights into common areas of inquiry.

Credit Approval Process: The process for these specialized industrial racking financing options is often more streamlined than for traditional loans. Lenders focus on the company’s overall cash flow health and the tangible nature of the asset being financed.

Inclusion of Ancillary Equipment: A significant advantage is the ability to create a turnkey solution. The industrial racking financing options can encompass not just the racking but also the necessary forklifts, Warehouse Management System (WMS) software, and conveyor systems, creating one seamless, integrated solution with a single payment.

Integration with Existing Assets: A professional audit will determine if existing, sound racking structures can be integrated into the new financed system. This can optimize the overall investment and reduce waste.

Tax and Accounting Implications: While specific advice must come from a qualified accountant, operating lease payments are typically treated as a fully deductible operating expense, which can offer a significant advantage over the depreciation of a purchased asset. Providers of industrial racking financing options are well-versed in these general principles across different regions.

The Future is Flexible: Aligning Warehouse Infrastructure with Business Agility

The global trend in logistics and supply chain management is unequivocally moving towards flexibility, resilience, and technology-driven optimization. The old model of static, capital-intensive infrastructure is incompatible with the demands of modern commerce. The future belongs to businesses that can adapt quickly, scale efficiently, and leverage partnerships to stay ahead. Adopting a strategic approach to industrial racking financing options is the most direct and intelligent path to building that agile, future-proof warehouse.

Conclusion: From Capital Barrier to Strategic Enabler

The conversation has shifted. The question is no longer if a business can afford to modernize its warehouse, but how it can afford not to, given the accessible industrial racking financing options available today. The financial innovation behind Zero-Capex Industrial Racking has dismantled the final barrier to operational excellence.

Companies can now simultaneously achieve two critical objectives: deploy a high-performance, safe, and scalable storage system that drives down operational costs, while preserving precious capital for other strategic growth initiatives. The hidden cost of inefficiency is a constant drain. The opportunity for transformation is immediate. By leveraging these sophisticated industrial racking financing options, businesses can stop deferring their growth and start realizing it.

Frequently Asked Questions (FAQs)

1: How does the credit approval process for a Zero-Capex racking solution work, and what are the typical requirements?

The process for these specialized industrial racking financing options is often more streamlined than for a traditional business loan. Lenders and lessors specializing in equipment finance focus on the company’s overall financial health, cash flow stability, and the fundamental strength of the business case. The tangible nature of the storage equipment itself provides security for the financier. This focus often results in higher approval rates for small and medium-sized businesses compared to standard bank loans, making these industrial racking financing options highly accessible.

2: Can I include ancillary equipment like forklifts, pallet trucks, or a Warehouse Management System (WMS) in the financing agreement?

Absolutely, and this is a key strategic advantage. The most effective industrial racking financing options are designed to create a fully integrated, turnkey solution. This means you can finance the entire ecosystem—the physical racking structures, the automated guided vehicles (AGVs/AMRs), the conveyor and sortation systems, and even the critical Warehouse Management System (WMS) software—under a single, cohesive financial agreement with one predictable monthly payment. This holistic approach ensures all components work in harmony and simplifies budgeting.

3: If I have an existing, partially usable racking system, can it be integrated or traded in for a new financed solution?

This is a very common and practical scenario. During the initial technical audit, our engineers will conduct a thorough assessment of your existing racking, evaluating its condition, compatibility with modern safety standards, and potential for integration. If components are sound and align with the new design, they can be incorporated. For equipment that is decommissioned, we can often facilitate a trade-in program or ensure its responsible recycling, with any recovered value being credited towards your new, financed solution, optimizing the overall investment in your industrial racking financing options.

4: How does the tax treatment of these payments typically work for businesses in different regions (e.g., Southeast Asia, Middle East)?

While we always strongly recommend consulting with a local qualified tax advisor for jurisdiction-specific guidance, the payments for operating leases under common industrial racking financing options are generally treated as a fully deductible operating expense (OPEX) in the year they are incurred. This can provide a significant tax advantage compared to the multi-year depreciation schedule of a purchased capital asset (CAPEX). Our financial partners have extensive experience structuring these industrial racking financing options across various international markets and can provide general insights based on prevailing practices.

5: What kind of performance guarantees or Service Level Agreements (SLAs) come with a financed automation system like an ASRS or AGV fleet?

When you finance a high-tech automation solution through reputable industrial racking financing options, it is backed by robust performance and maintenance guarantees. We stand by the operational uptime and throughput of our systems. Our Service Level Agreements (SLAs) clearly define guaranteed uptime percentages (e.g., 99.5%+), rapid response times for technical support, and include comprehensive preventative maintenance schedules. This ensures your automated operation runs smoothly and predictably from day one, protecting your productivity and providing peace of mind that your investment is secure.

Welcome to contact us, if you need warehouse rack CAD drawings. We can provide you with warehouse rack planning and design for free. Our email address is: jili@geelyracks.com